Weekly Earnings Review and Market Thoughts: $DDOG $TTD $HUBS & More

Weekly Earnings Review and Market Thoughts: $DDOG $TTD $HUBS & More

Another week of earnings in the books and we are almost across the finish line for 3Q. Revenue beats have been meek but earnings have come in strong as margins have held up better than expectations. The current earnings season is showing a more pronounced market reaction to earnings reports, both positive and negative. Companies that have beaten earnings expectations for 3Q are enjoying an average stock price increase of +1.1% around their earnings release, slightly more than the 5-year average of +0.9%. Conversely, those with negative surprises are facing harsher reactions, with an average price drop of -4.6%, almost double the 5-year average of -2.3%. At the sector level, Communication Services and Financials are leading in beating revenue estimates, while Utilities and Materials lag behind. The blended net profit margin for the S&P 500 stands at 12.1%, surpassing both the previous quarter and 5-year averages.

Consumer Discretionary and Information Technology sectors displayed robust growth. Standout performances from AMZN 0.00%↑ , ABNB 0.00%↑ , MSFT 0.00%↑ and INTC 0.00%↑ have been pivotal in driving this upward trajectory. Conversely, the Energy sector, despite high oil prices, reported a significant decline in YoY earnings, mainly due to lower oil prices compared to the previous year. Health Care also saw a downturn, with PFE 0.00%↑ and MRNA 0.00%↑ significantly contributing to the sector's earnings decline. Next week we are going to get a plethora of retailers reporting earnings which will give us a better read into how the consumer is doing in November.

DDOG 0.00%↑ 3Q was a pleasant surprise to investors, showcasing a company in full stride despite headwinds in other usage based names. The firm reported a 25% YoY revenue increase, hitting $548 million and surpassing expectations. This growth is particularly impressive considering the broader economic is still weak. Customer growth was strong rising to approximately 26,800, up from 22,200 last year with 3,130 having ARR over $100,000, accounting for 86% of the total ARR. FCF came in at $138 million, yielding a 25% margin. Billings were $607 million, a 30% YoY increase, and RPO stood at $1.45 billion, up 54% YoY. The improvement in their gross margin to 82.3% reflects strategic cloud cost efficiencies. Opex grew 17%, which was slower than revenue, resulting in a 24% operating margin. Q4 revenue between $564 million to $568 million, with FY 2023 revenue expected to range from $2.103 billion to $2.107 billion, which is still below where estimates were prior the cut in 2Q. Execution continues to be stellar with infrastructure monitoring ARR exceeding $1 billion and both APM and log management product surpassing $500 million. Despite the ongoing trend of cloud optimization, usage growth across the platform remained stable and consistent throughout Q3, mirroring the levels seen in Q1. Furthermore, the company reported an increase in new logo bookings YoY, with a record number of deals exceeding $100,000. Product development and innovation are at the heart of Datadog's growth strategy and they have done a tremendous job transitioning from a point solution to a platform by expanding APM capabilities, introduction of Flex logs, and the launch of DevSecOps packages.

There was nothing incrementally new from the quarterly results and DDOG saw a relief rally as sentiment for usage based SaaS names was extremally low. My thoughts on the valuation haven’t changed from what I wrote after the 2Q results . DDOG is now trading near my upper bound valuation and chasers should be cautious.

HUBS 0.00%↑ expectations were low going into ER and they revealed results that surpassed those expectations. Revenue reached $443 million, marking a 24% YoY increase in constant currency and 26% as reported. This upsurge was primarily driven by a strong subscription revenue of $429 million, up 25% YoY. Domestic revenue grew by 22% YoY, while international revenue saw a 26% increase in constant currency, contributing to 47% of total revenue. Total customers rose to over 194,000, a 22% YoY increase, with 9,100 net new customers added in Q3 with 50%+ of installed base now on 3+ hubs.. Non-GAAP Operating Income stood at $71.2 million, translating to a 16% operating margin, up 700 basis points YoY, benefiting from strategic cost optimizations. FCF was $65 million, representing a 12% FCF margin. Gross retention remained in the high 80s and NRR saw a slight increase QoQ. NRR still faces headwinds due to the macro environment. Management remains focused on sustaining NRR above 100%. HubSpot AI, launched at Inbound 2022, is showing early positive signs, with significant adoption among enterprise and pro customers. The focus is on expanding AI use cases and increasing user adoption. 40% of enterprise customers have already used HubSpot AI features, along with 20% of Pro customers. Around 2/3 of AI users are leveraging AI assistance for crafting marketing emails and blogs. Social publishing is a sticky use case. Acquired Clearbit for $150 million in cash, a strategic move to enhance its CRM offering and AI capabilities. They are not looking to enter a new database business with Clearbit, focused on accelerating customer platform vision as they continue to operate in an open ecosystem.

I’m a big fan of HUBS, and Dharmesh in particular, but even after the recent pullback shares are not cheap trading at 55x ‘24 FCF. HUBS should do ~$1B in FCF by ‘27 and 25-30x FCF multiple seems reasonable, putting the shares at ~$350 using a 10% discount rate.

AYX 0.00%↑ has made a notable comeback in Q3, showcasing solid results and a strategic shift in sales and operational execution. This period marked a significant improvement from the challenges faced earlier in the year, with Alteryx demonstrating robust growth in ARR, effective cost control, and a burgeoning partner ecosystem. ARR grew 21% YoY to $914 million, surpassing guidance by $9 million. Revenue reached $232 million, exceeding expectations by $20 million. Non-GAAP operating income was $36 million, significantly above the guidance by $30 million, a result of improved sales productivity and disciplined spending. The customer base saw substantial growth with a 20% increase in $250K+ ARR customers and over 30% in $1M+ ARR customers and over 50% of new ACV in Q3 was driven by Alteryx’s expanding partner network. NRR was solid coming in at 119% overall and 130% for Global 2000 customers. The forecast for Q4 suggests a conservative approach, with net new ARR expected to be lower YoY.

3Q results signifies a successful turnaround, characterized by improved sales execution, growing customer base, and a disciplined operational approach. The firm's efforts in broadening its partner base, upgrading its offerings with AI and cloud technology, and keeping strong customer retention are positive signs. However, lingering concerns about Q4 projections and my reservations about Alteryx's competitive standing and the overall compelling nature of its value proposition temper my enthusiasm. The company's execution and its reasonable valuation are noteworthy, yet I remain cautious. I feel it's prudent to observe a few more quarters of consistent performance to fully gauge the company's potential in the competitive tech landscape before considering a deeper interest.

AMPL 0.00%↑ results modestly exceeded expectations, thanks to effective management of churn rates, which, while still elevated, showed a quarter-over-quarter decrease in absolute dollar terms. Amplitude posted a 15% YoY revenue growth, totaling $70.6 million, which was slightly higher than the $70.0 million expected by the Street. ARR increased by 12% YoY to $273 million, marking a net new ARR of $5 million for the quarter and posted its first quarter of positive operating income, with non-GAAP operating income at $2.8 million. This represents a 4% margin and a significant beat over the consensus estimate of $0.7 million. NRR dipped below 100% to 99%, reflecting ongoing challenges with churn. They raised its FY23 revenue guidance to $276.5 million, slightly above the Street's forecast of $274.9 million.

Results were fine and the valuation, at 3x sales, is compelling but the only way shareholder will generate an attractive return is via a takeover. AMPL falls into the category of SaaS companies that provide point solution and will get left behind as the industry looks to adopt a platform approach that will allow them to consolidate vendors.

TTD 0.00%↑ reported strong results with a 25% YoY revenue increase, reaching $493 million. Adjusted EBITDA stood at $200 million, 40% of revenue, with a free cash flow of $184 million. Excluding political ads, growth was approximately 27%. CTV continues as the fastest growing channel, driving overall growth alongside retail media. North America contributed 87% of revenue, with international segments growing slightly faster, representing 13%. Key growth drivers include the shift to CTV, advances in measurement and attribution via retail media, widespread adoption of UID2, and global expansion. JVPs, reflecting deep innovation partnerships, are significant, with multi-year deals exceeding $1 billion in spend. These partnerships underscore a trend towards more flexible, agile, and data-driven advertising. CTV ad inventory is increasingly shifting to auction-based programmatic buying, enhancing efficiency, targeting, and measurement. Premium content owners, including Disney, are moving more inventory to programmatic channels. The platform is also integrating more live sports content. The adoption of UID2 is accelerating, offering better relevance without data sharing, and early adopters are witnessing substantial revenue increases. AI integration across the platform is enhancing bidding optimization, pricing, value assessment, and ad relevance, promising further performance improvements into 2024.

Late Q3 and early Q4 saw some advertiser caution due to macroeconomic factors, impacting sectors like auto and consumer electronics, leading to a weak 4Q guide that missed consensus by $30M on the topline and $20M in EBITDA. This weak guide saw the stock crater almost 30% at the lows before rebounding and finishing down 17% the next day. Here is what I wrote last quarter about TTD:

So what’s priced in? If we assume analyst estimates are credible and revenue reaches ~$4.5B in ‘27 with FCF margins of 35%, as FCF conversion moves closer to adj EBITDA, we would need TTD to trade at 35x FCF and an EV of $55B in order to generate 10% CAGR over the next 4-5 years. This assumes no dilution, which would require even more heroic assumptions in order to generate a double digit CAGR.

In summary, while TTD is undeniably a stellar firm with a top tier management team, its current $75/share valuation leaves little margin for hiccups in its growth trajectory. TTD trade down to $50-$60/share in ‘22 and ‘23, which is a much more reasonable level to accumulate share.

The stock decline was simple, valuation was extremally high and any short term hiccup was bound to send shares crashing lower. From an execution point, TTD continues to to do exceptionally well and I believe the guide miss was all macro and not related to any competitive pressure. The r/r is now much more compelling and a dip to the 50-55 range can be used as an opportunity to accumulate shares.

UBER 0.00%↑ recent earnings have showcased a company in full stride, leveraging both its core and emerging services to carve out a dominant position in the mobility sector. The company's growth algorithm, underpinned by strong unit economics and disciplined growth strategies, sets the stage for robust free cash flow growth in the coming years. Gross Bookings surged by 21% YoY to $35.3 billion, with Adjusted EBITDA hitting $1.1 billion and net income at $221 million. These results align with the top end of the company's guidance. Mobility segment Gross Bookings climbed to $17.9 billion, up 31% YoY. while the Delivery segment saw a rise to $16.1 billion, up 18% YoY. New Verticals, encompassing grocery and other services, grew by 46% YoY.

Mobility trends have caught up to pre-Covid levels so questions around growth in Mobility have emerged. The APAC and LatAm regions have shown remarkable growth propelled Products like hailable taxis and 2-wheelers, particularly in markets like Japan, South Korea, Brazil, and other LatAm countries. These new offerings are instrumental in driving growth in these regions. Untapped high GDP markets like Germany, Spain, Argentina, Japan and South Korea is another avenue for growth but will take investment to compete in those markets. Initiatives like hailables, 3-wheelers, 2-wheelers, Uber for Business, UberX Share, high-capacity vehicles, and Reserve collectively contribute $9 billion, growing over 80% year-on-year. Uber One, with 15 million members, is a key element in increasing user spend and retention. Members spend four times more than non-members, and Uber aims to offer both financial and non-financial benefits to enhance member experience.

Uber's moat is reinforced by significantly reduced competition and its vast scale, making market entry challenging for new players. Additionally, its immense user data pool presents a formidable advantage in AI, potentially driving further innovation and market leadership. Uber is currently trading at 21x ‘24 FCF estimates and there is a credible path for FCF to double to over $10B by ‘28. Keeping the multiple constant, which can be justified given their advantageous competitive position, and stock can double over the next 5-years generating a double digit CAGR for investors.

APP 0.00%↑ delivered another blow out quarter showcasing strong execution and significant share gains for the company's ad network, powered by the AXON machine learning engine. Total revenue beat expectations by 9%, ad network revenue by 12%, and EBITDA by a whopping 18%. The core AppDiscovery DSP product was a standout, driving most of the 65% YoY growth in the ad network and the 72% segment EBITDA margins were impressive – a testament to the cash flow potential of APP's business model (they mentioned EBITDA to FCF conversion is around 50%). The Apps segment saw a welcome resurgence, marking the first growth since 4Q’21. Despite increased marketing investments, the segment maintained a solid 15% margin. It seems APP has successfully restructured this segment, focusing on its financial rather than strategic value. APP's 4Q revenue growth forecast at 31% YoY shows management's confidence in AXON's ability to further drive share gains for AppDiscovery. Projections suggest a staggering 78% YoY growth rate for AppDiscovery by the end of '23. AXON 2 hit a significant milestone in with the integration of their CTV. As AXON 2 evolves and scales, it's becoming smarter, and they are continuously fine-tuning it for better results.

This quarter reinforced APPs tremendous execution and enviable position in the ad tech space. My thinking is the same as last Q, and APP is still reasonably priced given the level of execution but is no longer in bargain territory. You can look at my 2Q write up to get my thoughts on the valuation. APP Valuation

TOST 0.00%↑ results painted a mixed picture with revenue growth slowing while adding over 6.5K locations during the quarter. ARR witnessed a 40% YoY increase, hitting $1.2 billion and adjusted EBITDA hit $35 million. Subscription revenue grew by 46%, driven by the uptake of their software products while FinTech gross profit increased by 36%, primarily from credit card processing fees. GPV per location showed some weakness, SaaS ARPU growth is guided lower, and 4Q revenue forecast came in below expectations as macro factors impact consumer behavior. The company is constantly enhancing its platform, adding software modules to cater to diverse restaurant types, including those with retail elements, bakeries, cafes, and hotel food services. This expansion not only diversifies their offering but also deepens customer engagement. Even after the pullback TOST doesn’t look optically cheap but I think they have immense potential to dominate the US restaurant technology market as their focused, restaurant-friendly products, and effective sales strategies position them well for sustained growth. Short term fluctuations will be driven by consumer behavior and resurant spend but the long-term value of their payment processing and steady software subscription revenue is significant. I initiated a starter position and will continue to monitor progress and macro headwinds and while there are short-term challenges, the company's long-term growth trajectory remains promising.

GFS 0.00%↑ reported solid results showcasing resilience and strategic agility in a period marked by economic and geopolitical volatility. Despite the challenges performance aligns with the upper echelon of their guidance, indicating a robust management approach amidst a turbulent market. Revenues climbed to $1.85B, with adjusted gross margin of 29.2%, surpassing previous guidance, thanks to manufacturing optimizations and customer volume adjustments. Inventory is anticipated to remain elevated through the end of 2023 and into 2024 affected by demand in sectors like mobile devices and consumer electronics. They are engaging with customers to manage inventory adjustments without jeopardizing long-term agreements. This has led to some underutilization charges, expected to continue into Q4. The company is optimistic about a return to YoY growth in 2024, contingent on inventory reductions and demand recovery, especially in consumer-centric markets.

They are experiencing resilient demand in sectors like automotive, industrial IoT, and aerospace and defense, unveiling new partnerships and product developments, tracking to achieve $1 billion in automotive end market revenue in 2023. Significant progress has been made with its 22FDX platform for IoT and launched an advanced RF technology platform. They've also secured a 10-year contract with the U.S. Department of Defense for secure semiconductors. The company is targeting reduced capital expenditures in 2024, expected to be lower than 2023, positively impacting free cash flow while still expanding its global manufacturing footprint, including a $4 billion investment in Singapore, while remaining disciplined in capacity addition. Pricing for new LTSA wins remains accretive, especially in single-source differentiated offerings. The pricing for 2023 is projected to be flat to slightly up YoY. FCF is expected to inflect in ‘24 on the back of reduced capex spend. Shares are not expensive at 16x ‘24 FCF but my interest in a capex intensive foundry is limited and I would rather own TSM.

GPRO 0.00%↑ represents an interesting opportunity with a subscriber base of 2.5 million generating almost $100 million in high-margin revenue, up 20% YoY, GoPro's situation is intriguing, to say the least. The company's enterprise value of approximately $350 million, bolstered by around $80 million in net cash and about $1 billion in annual product sales, paints a picture of a business with untapped potential. But beneath this facade lies a history of struggling to find consistent growth levers and a narrative of continual strategic pivots. GoPro is once again shifting gears, this time placing more emphasis on lower-priced introductory products through the retail sales channel. This move is not without its trade-offs. In the short term, GMs are likely to feel the pressure. However, management exudes confidence that these margins will improve towards the latter half of 2024, fueled by reduced costs of goods sold for these entry-level models. This strategy, if successful, could re-engineer top-line growth and enhance FCF, potentially doubling or tripling the stock value in a relatively short time frame.

Despite management's optimism, I’m doubtful about the feasibility of expanding GM to the projected levels. GoPro's products, inherently discretionary in nature, face vulnerability to economic downturns. GoPro's pivot towards more economically accessible products is a double-edged sword. On one hand, it broadens the market reach, potentially driving unit sales. On the other, it ties the company's fortunes more closely to the whims of a consumer base that is highly sensitive to macroeconomic shifts. In an economic slowdown, discretionary spending is often the first to be curtailed, and GoPro's products could be squarely in the crosshairs of such consumer restraint. The unit economics of GoPro's subscription model merit a closer examination. With an attach rate of 40%, first-year renewal rates hovering between 60-65%, and second-year renewals at 70-75%, the company is losing over half of its subscribers within two years. This attrition rate raises questions about the perceived value of the subscription service. Is it truly resonating with users, or is it seen as a non-essential add-on?

The success of their latest strategic pivot hinges on several critical factors: the ability to scale up unit sales without proportionately escalating costs, navigating the delicate balance between premium and entry-level products, and enhancing the perceived value of their subscription service. I will adopt a wait-and-see approach with GoPro. The company's story is compelling, and its potential for rapid growth is undeniable. Yet, the skepticism surrounding its ability to expand gross margins and the overall economic sensitivity of its consumer base cannot be overlooked.

AXON 0.00%↑ delivered another strong quarter, marking its seventh consecutive quarter of 30% YoY growth. This consistent growth, reflecting strong demand across products and end markets, was in line with investor expectations, reinforcing our positive outlook on Axon's competitive and portfolio positioning. Despite this, we recommend waiting for more favorable entry points before investing. Taser 10 continues its momentum with order rates year-to-date outpacing the TASER 7 rollout by four times and a 50% quarter-over-quarter increase in demand. Federal deals contributed significantly, with five of the top ten deals in 3Q coming from this Federal. In 4Q Revenue is expected to be between $417-420 million, with gross margins slightly below 3Q levels and EBITDA margin around 20%. Axon's unique position, leveraging the early stages of a product cycle and an increasing mix of software/subscription services, places it favorably in markets with resilient spending trends. This is particularly notable against the backdrop of broader Networking & Hardware market trends. The company’s solid revenue guide for Q4 2023 and the potential for margin improvement next year reinforce our confidence in Axon’s prospects. There really isn’t much fault to be found in the recent Axon performance but valuation is keeping me on the sidelines. I’ll keep watching the stock hoping for a better entry point while kicking myself for selling down this position way too soon.

Alternative Asset Managers reported results and overall the group continues to execute in what is a tough macro environment for them. Several themes have been emerging over the last few years and thats Alt managers doubling down on insurance and private wealth. CG 0.00%↑ reported $382 billion in AUM and DE of $382M. Despite headwinds, Carlyle raised $6.3 billion this quarter and expects a strong Q4. While transaction and advisory fees dipped, management fees remain steady, hinting at a potential uptick in the coming quarter. The firm's expense management, notably the $40 million run rate savings, aligns with their goal of operational excellence without compromising growth.

KKR 0.00%↑ posted very good results with fees reaching $759 million, marking a robust 13% YoY growth and FRE margin reaching 61.7%, remaining above 60% for 12 quarters. Global Atlantic contributed $210 million in pretax earnings and expecting a $13 billion AUM increase from the MetLife deal. Global Atlantic's assets surged from $72 billion to $158 billion since 2020. They are doubling realized performance income, reflecting strategic and timely exits. They raised $14 billion in a challenging market, with a strategic focus on private wealth and climate investments. Making inroads into healthcare investments by partnering with Catalio. They are aiming to double Distributable Earnings by 2026, leveraging flagship fund raising and margin improvements.

The real star for me was BAM 0.00%↑, yet the market refuses to show it any love. FRE Increased to $565 million, an 8% YoY rise. BAM capital base is sticky as 86% of their capital is long-term or perpetual, providing a stable financial base. They raised $61 billion this year, with $26 billion in 3Q alone, steering towards a $150 billion target. They are aiming for slower expense growth in 2024 with significant operating leverage which should drive significant dividend increases going forward. BAM is sitting a dry powder which creates capacity to be buyers in a downturn. I find shares trading in the low 30s to be very attractive given the long term DEs and dividend growth potential. As always, while surprises can occur in the short term, BAM's well-structured business model provides a buffer against most negative shocks, making it a prudent choice for those looking for steady, long-term gains.

Last week I talked about expecting markets to trade in a narrow range after a huge reversal from oversold conditions. I was right, until the weird up move on Friday without much catalyst to speak of. SPX finished the week up 1.3% and NDX was up 2.8%, with almost all of the move occurring on Friday. Conditions quickly moved from oversold to overbought levels. My year end rally thesis played out much faster and more violent than I anticipated and I think the bulk of the move has happened and we will most likely stay range bound between 4400 and 4500.

In terms of industries, semis bounced hard, maintaining relative strength amidst market fluctuations. This resilience could be attributed to several factors, such as the ongoing global demand for technology and electronics, despite supply chain issues. Semiconductor stocks might continue to benefit from these trends. The lag in solar, regional banks, airlines, and office REITs appears rooted in distinct industry-specific challenges. I think the YTD trend of semis, software and home builders leading the way higher while solar, regional banks, airline and office REITs will continue to lag as there are no near term catalyst that will cause fundamentals to improve. Solar and airlines might need more robust policy support or a shift in economic conditions. Regional banks could be sensitive to further interest rate movements and economic health, while office REITs face a longer-term structural change in how office spaces are used.

On the economic side, we have inflation readings with CPI results on Tuesday and PPI on Thursday. This could create some volatility but I don’t think they will come in much different from current consensus estimates and the equity markets have moved past worrying about inflation readings. Tuesdays retail sales will give us a better look at the consumer and Thursdays Industrial Production reading on manufacturing output. All of these readings are lagging indicators so i don’t put much emphasis on them given that the market is always looking 6-12 months forward. Heading into 2024 the consumer will start to get squeezed as things like tighter policies, less easy credit, and a bit of a dip in labor income are making people think twice before splurging. Weaker consumer spending will be offset by the comeback of business investment a job market that while cooling will continue to stay strong relative to historical standards. Mental flexibility and adaptability in the current economic environment is critical. The wide range of possible outcomes for 2024 necessitates a dynamic investment approach, ready to adjust strategies based on emerging data and trends. Given these varied and complex economic signals, investors must remain vigilant, continuously analyzing new data and adjusting their thesis accordingly. The interplay between consumer behavior, monetary policy, and geopolitical factors will be key in shaping the economic landscape in 2024.

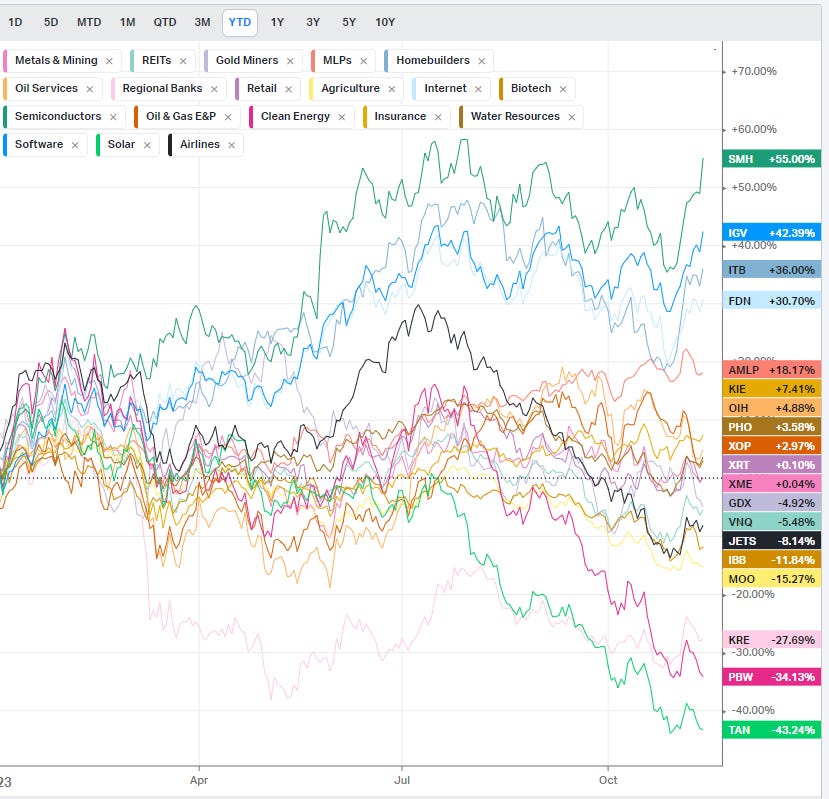

The NY FED released the Household Debt and Credit report which showed that credit card debt transitioning into delinquency continued to rise and is now well above pre-covid levels. According to the U of Michigan consumer sentiment continues to decline on the back of higher rates. While not definitive, these are all signs pointing to a consumer that may be exhausting themselves and are ready to close their wallets in 2024, especially if rates continue to stay high while geopolitical tension spill into local political unrest.

Interesting links:

https://www.semianalysis.com/p/nvidias-new-china-ai-chips-circumvent

How to Craft a Winning Investment Process and Spot World-Class Companies

Hi Elliot, how do you make your evaluation model to know whether or not you feel conformable to buy or sell a SaaS co? I don't feel like you are doing a full DCF model to take those decision but more like 5y fwrd rev estime*fcf margins*multiple*discount/share count*dilution^year. Not sure if i'm clear lmao, anyway my question is more about what multiple do you think are right for some SaaS etc since they are valuated on EV/NTM S or EV/NTM FCF.. Thanks for your time!