$ZM 3Q Results

ZM 0.00%↑ posted their standard 1.5%-2% topline beat but it was profitability and FCF that really exceeded expectations. Sales climbed by 3% YoY to $1.14 billion, edging past expectations by 1.6%. The FCF margin hit 40%, translating to $453 million, bolstered by efficient collections, reductions in opex, and the interest income from their substantial $6.5 billion cash and securities holdings.

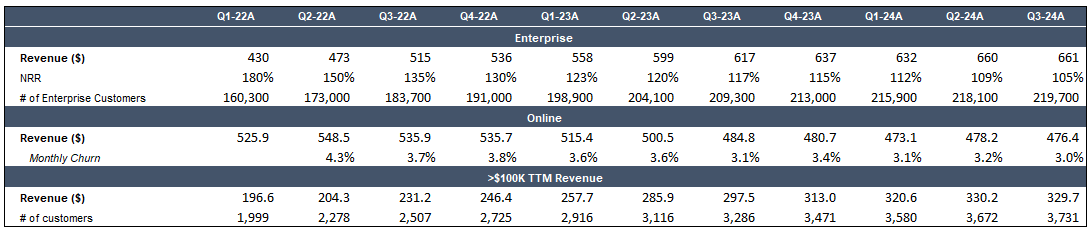

Zoom's product suite, especially its Phone and AI Companion, continues to make impressive strides. The Phone service has now reached approximately 7 million paid seats, and the AI Companion is gaining significant traction. The company's ongoing product expansion, notably in the Phone and Contact Center sectors, is noteworthy. With a jump from 500 to 700 Contact Center customers in the last quarter, the potential for further expansion is evident. In a similar vein, Zoom One bundles incorporating Zoom Phone have skyrocketed by 330% YoY, showcasing the platform's increasing allure and a record-low churn rate in the Online segment, signaling stronger customer loyalty and retention.

The growth in Enterprise customers by 5% year-over-year is a positive, yet DBNER has seen a notable slowdown to 105% from 109% in the previous quarter and 117% last year. Billings were somewhat tepid, attributed to customer preferences for shorter payment terms ( PANW 0.00%↑ gave the same reason), leveraging higher short-term rates for better working capital yield. This is reflected in the disparity between the robust 10% year-over-year growth in RPO and the billings figures. The customer base spending over $100K increased by 59 sequentially and 445 year-over-year to 3,731, though revenue saw a slight QoQ dip. Despite not observing an uptick in churn, the company notes a trend of down-selling as customers adjust headcounts due to a softer macroeconomic environment, countering this impact through the sale of more bundled offerings.

Zoom's transition from a high-growth tech darling to a more mature, steady entity is unmistakable. Its metamorphosis into a verb reflects its deep integration into our daily lives, especially for SMBs and larger corporations outside MSFT 0.00%↑ Teams sphere. Zoom remains a top choice for hybrid work environments. However, growth dynamics have shifted. Zoom is evolving into a low-growth, high-margin business. Recognizing this new phase, it's time for strategic financial maneuvers. With a hefty $6.5 billion in cash and securities, Zoom could effectively use about half of this reserve to repurchase nearly 15% of its outstanding shares. Implementing a dividend or buyback policy that directs all FCF to shareholders could be a wise move. Such a strategy may attract investors seeking yield and robust capital returns, offering a fresh perspective on Zoom. Currently, Zoom's over 10% FCF yield seems to have factored in much of the skepticism surrounding its growth potential. While there's no immediate catalyst on the horizon to significantly move the stock, patient investors have options. Strategies like covered calls or writing naked puts could be employed to generate yield in the interim, biding time until a potential stock catalyst emerges, possibly as early as the first quarter. This approach offers a way to navigate Zoom's current landscape while awaiting future developments.