Is TLT The Place To Hide in 2024?

The recent bond market downturn seemingly lays bare a chance for discerning investors to hedge against impending economic slowdown and subpar forward equity market performance, particularly when juxtaposing the 10-year yield with the ERP. This shift, spurred by tumultuous bond market dynamics, prompts a venture into macro analysis—a domain often eclipsed by a personal penchant for individual equity security analysis. The evolving discourse on long-term rates vis-a-vis equity markets underscores a complicated and nuanced interplay, requiring a deeper comprehension to adeptly steer through the current landscape.

The idea of leaning towards long duration bonds now revolves around a likely return to a low-inflation, low-rate setting like before the pandemic. If this happens, the relationship between stocks and bonds, which briefly turned positive with rising inflation and interest rates, will likely go back to being negative. This change could see real yields drop below 1%, with 10-year rates steadying around 2-3%.

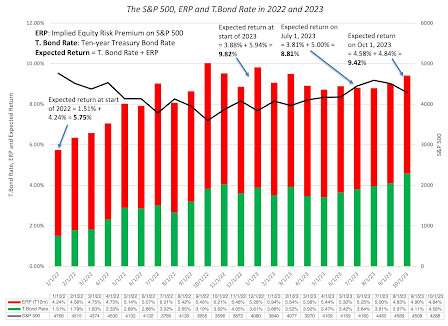

Source: https://aswathdamodaran.blogspot.com/2023/10/market-bipolarit-exuberance-versus.html

Equities, conversely, seem to have wholeheartedly imbibed a soft landing narrative, inflating multiples by 20% since last October. Yet, this narrative might be treading on fragile ground. The U.S. stands at the cusp of a notable economic downshift as we voyage into 2024. Fiscal stimulus is foreseen to decelerate over the next half-year, removing a key support for the economy. In tandem, the stark surge in labor productivity growth is approaching its mean reversion threshold. The recent change in monetary policy perception as the market started pricing in short term rates to stay higher for longer is another concern, likely to slow down economic activity while pushing down inflation.

The extra savings that consumers had during the pandemic, which helped lower and middle-income families handle inflation and maintain their lifestyles, is almost gone. Rising delinquency rates on credit cards and auto loans, the return of student loan payments, rising unemployment, and ongoing price increases over the last few years indicate a consumer who will be more cautious in 2024. In contrast, long-dated bonds are emerging as a good value and remain relatively under-owned. The yield on 10-year TIPS is around 2.4%, a bit high from a historical standpoint, offering a solid option for investors looking to steer clear of the equity storm.

As the fiscal and monetary boosts that drove the U.S. economy begin to fade, the equity market could find itself in a tough spot, especially if the expected soft landing turns into a rough one. Long-dated bonds, with their current yield levels, provide a safe haven for investors in this scenario, offering protection against potential drops in the stock market, and a decent return if the world is heading back to low inflation and low rates. For long only investors, considering some exposure to long-duration bonds seems wise given the unclear outlook for 2024. The path ahead is full of uncertainties, and a sensible allocation to long-duration bonds could provide a stabilizing factor by preserving capital to be redeployed at more attractive levels, leading to a stronger portfolio amidst changing conditions.

For traders looking to bet on duration, this is a trickier proposition since timing is key. A concern regarding long-duration bonds because of the growing U.S. budget deficits and national debt has emerged as a recent narrative for the reason yields will continue to climb higher. The worry is that the excess bond supply, resulting from the U.S.’s constant budgetary overspending, might have exceeded or is close to exceeding the demand from both domestic and international investors. This imbalance could keep pushing bond yields up, ushering in an age of austerity for governments. A recent conversation with former Treasury Secretary Larry Summers and comments made by Bill Ackman echoed this concern, hinting at a likely rise in steady-state real interest rates due to a continuous increase in America's structural deficit.

This argument seems plausible and deserves a closer look. However, a dive into historical data doesn’t fully support the idea of a continuous lack of buyers. Despite growing budget deficits since the early 2000s, real bond yields have been dipping. A similar trend is seen in Japan, despite fiscal deficits rising since the early 1990s, real interest rates have been on a downward trend. Looking back, widening budget deficits across most developed nations over the last two decades show a common problem: a surplus of private sector savings forcing governments to borrow and spend to keep the economy balanced.

This excess savings issue also explains the long-lasting low inflation seen across high-income economies before the pandemic. The key question moving forward is about the balance of savings and investment. Deficit levels and the current fiscal policy is unsustainable and reversing fiscal overspending is a politically tricky task. It’s always possible that this time is different and the debt narrative provides a valid counter-argument, historical evidence casts doubt on a direct link between rising deficits and rising real bond yields.

Another potential scenario may unfold if credit markets face turmoil, compelling the Federal Reserve to loosen monetary policy prior to fully tackling inflation. This could trigger a rebound in inflation as the Federal Reserve's credibility wanes, catalyzing a rise in long-term real yields. We might be veering towards a 1970s-esque scenario where a resurgent inflation, paired with a less credible Federal Reserve, necessitates significantly higher rate hikes to regain control and thwart entrenched inflation. Should this narrative materialize, vigilant investors will find ample indicators to trim down their exposure to long-term bonds, thus mitigating the fallout from this economic tempest.

The current r/r profile for long-term bonds appears compelling, notably within the framework of holistic portfolio construction. The potential for capital preservation and income generation amid economic uncertainties could enhance portfolio resilience, while offering a counterbalance to equity market volatility. This strategic allocation might be prudent for investors aiming for a diversified asset mix to navigate through varying market phases.

Thoughts on Reemerging Banking Crisis:

The ongoing dip in bank stocks signals that the issues which troubled the banking sector earlier this year are still present. Higher MM rates are drawing deposits away from banks, while their assets face challenges with rising bond yields and a persistent slump in office CRE. This situation mirrors past troubles, where a misalignment between liabilities and assets triggered banking hurdles. On the liability side, regional banks were losing deposits to higher-yielding money market funds. Simultaneously, banks' assets were stressed due to bond sell-offs and the decline in commercial real estate values, especially office spaces.

Since the initial hiccups at SVB surfaced, the Fed has hiked short-term interest rates by 75bps and indicated intentions to maintain them at elevated levels for an extended period. This scenario continues to fuel the shift towards higher-yielding MM funds, leaving commercial banks grappling to retain their deposits. The asset side of the balance sheet hasn’t seen any relief either. The recent tumble in rates has likely exacerbated unrealized MTM losses for banks.

A key issue with SVB was its significant investment in long-dated government bonds at very low yields. When faced with unprecedented deposit outflows, SVB needed to sell these bonds and realize losses. To alleviate such pressures, the Fed introduced the Bank Treasury Financing Program in mid-March. This program allows banks to pledge U.S. Treasuries, agency debt, and mortgage-backed securities at face value for liquidity, even if these bonds are trading below face value. Hence, banks can borrow at rates higher than the value of their posted collateral. The sustained high borrowing from BTFP indicates that the fundamental challenges haven't been mitigated since its introduction. A further uptick in BTFP borrowing could signal escalating stress, especially following the recent bond market turmoil.

The BTFP by the Fed acts as a crucial buffer against the financial strain encountered by SVB and other regional banks this year. Had this facility been available earlier, SVB could have avoided steep losses on its bond portfolio by pledging bonds to the Fed at face value to handle deposit outflows and mitigate the panic. The narrative around the downfall of banks is exaggerated, but ongoing bond market woes and tensions in CRE continue to impede regional banks from extending credit, thereby tightening financial conditions.

Money and credit form the essential foundation of an economy. Restricting their flow makes the economy susceptible to risks. It becomes challenging to boost nominal spending when the M2 money supply and credit availability are shrinking. This situation accentuates the necessity for measures such as BTFP that can address the underlying issues facing banks, ensuring the smooth flow of credit and money to foster economic stability and growth.