GOOG Earnings: Business is Solid, Stock is Cheap, but Macro + Search Risk Keep It Grounded

GOOG put up a strong Q1with revenue growing 14% y/y in constant currency, GAAP profit was up 20%, and margins came in better than expected. Nearly every major business line posted solid growth, and despite all the noise around AI disrupting search, there’s still no real evidence of cannibalization. But the market didn’t react much. The reason? Google flagged a slower start to Q2 and reminded investors of two headwinds: macro uncertainty and the end of the de minimis rule (which impacts cheap D2C sellers from APAC). Combine that with $75B in CapEx spending this year, which is going to blow out depreciation across the P&L, and it’s hard to get investors excited in the short term. Still, strip out the noise, and you have a business that’s growing 10–12% y/y with 33%+ GAAP margins, a highly defensible search franchise, and a stock trading at HDD ‘26 EPS. That’s cheap, especially if you believe Google retains most of its search economics and can slow CapEx growth over the next couple years.

Search: No Sign of Structural Erosion (Yet)

Search revenue grew 10% y/y, driven mainly by pricing (paid clicks were up just 2%). That’s both good and bad as monetization is clearly still strong, but demand softness is starting to creep in. Management gave vague commentary on Q2 trends, but flagged some weakness from tariffs and a tougher macro backdrop. The AI conversation continues to hang over search. On the one hand, AI Overviews are now being shown to 1.5 billion users per month and Google claims monetization is approximately the same as traditional search results. That’s a big deal and it means the core economics are holding, at least for now. They’re also rolling out AI Mode inside Search, which allows for more complex, multi-step queries. Early feedback is positive. These queries tend to be 2x longer and more nuanced, which creates opportunity to expand the surface area for monetization, but it’s early. One underrated detail is visual and multimodal search is growing fast. Circle to Search is now on 250M+ devices, usage was up 40% q/q, and Lens query growth was strong. It’s still small, but this is how Google continues to expand its moat by staying at the center of new types of query behavior. Another subtle tailwind here is the quiet decline of Google’s Network business which has now shrunk for 11 straight quarters. This used to be a TAC-heavy, low-margin drag on profitability. Now, as it fades into irrelevance, Google’s ad revenue mix is actually improving. That’s helping push Google Services margins to 42.3% this quarter, the highest ever. Bottom line: search isn’t broken. The monetization model is holding up, usage is stable, and Google is evolving the product. The bear case that GenAI disrupts the core business is still mostly theoretical. And if it doesn’t materialize in the next 1–2 years, the stock is just too cheap.

YouTube: Still Growing, and Subscriptions Are Quietly Booming

YouTube advertising was up 10% y/y, and Shorts engagement grew 20% q/q. Those are good numbers. Management also said the number of YouTube podcast users hit 1B monthly actives. That’s an underappreciated distribution engine that will matter more over time. On the subscription side, YouTube Music + Premium hit 125M subscribers globally (though this includes trials), and overall subscriptions across Alphabet hit 270M. That bucket, now grouped under Subscriptions, Platforms & Devices, grew 19% y/y and actually generated more revenue than YouTube ads in Q1. That’s a big shift. Back in Q1’22, both segments were about equal. Now, subs have pulled ahead. This matters more than it seems. Subscriptions are recurring, high-margin, and sticky. If Google can start layering AI-powered features like personal assistants, enhanced search tools, or AI-generated productivity features into Google One and YouTube Premium, it opens the door to re-pricing the whole bundle. That could turn this from an overlooked segment into a legitimate multi-billion dollar EBIT engine. YouTube continues to benefit from its unique position as the only platform that can serve content across short-form, long-form, live, podcast, and music and it’s integrated into Google’s broader ecosystem. Monetization is still ramping, especially on Shorts, and they’re pushing harder into branded/reservation-style ad deals. There’s no sign of weakness here. If anything, the story is getting better.

Google Cloud: Growing Fast, Now Profitable, but Capacity-Limited

What’s underappreciated is how fast Google Cloud is scaling while already showing margin leverage. It just crossed a ~$50B run-rate growing nearly 30% y/y, and it's doing that with 18% operating margins, up from low single digits just a year ago. That’s impressive in a market where hyperscaler competition is intense and pricing pressure is real. Microsoft has a strong enterprise foothold, and Amazon remains dominant in IaaS, but Google is carving out its lane by going deep on AI infrastructure, open tooling (Vertex AI, open model support), and hybrid deployments (Sovereign Cloud, Distributed Cloud). Where Google could pull ahead is in next-gen AI infrastructure. Their in-house TPUs (now in Gen 7 with Ironwood) are optimized for inference at scale and deliver 10x compute performance with 2x better power efficiency. That translates into a real cost advantage in AI training and inference workloads, especially at scale. Combine that with their open model support, Vertex AI tooling, and distributed cloud options, and you get a compelling stack that’s already attracting high-value use cases. If Google can keep ramping capacity and converting AI demand into enterprise stickiness, Cloud could evolve into a core monetization layer not just for enterprise, but for Alphabet’s broader AI ecosystem.

AI & Gemini: Product Velocity Is Back, and It’s Paying Off Internally

This was the most encouraging quarter yet for Google’s AI story. Gemini 2.5 is now integrated across Search, YouTube, Android, and Workspace. Every product with 500M+ users now uses Gemini under the hood. The product team seems to have finally found its rhythm with Gemini Live, Circle to Search, image/video generation tools, and AI agents are shipping fast and getting solid feedback. What’s not being talked about enough is how much internal productivity lift Google is already seeing from AI. 30%+ of Google’s own code commits now involve AI-generated suggestions, up from 25% just a few months ago. These tools are actively reducing developer cycle time and improving throughput. Multiply that impact across other functions like customer service, finance, legal, and marketing and you have real margin leverage coming from AI, not just headline buzz. This is the stealth version of AI monetization, not via user pricing, but via internal operating leverage. Few other companies are positioned to get this kind of first-party efficiency benefit at scale. If this continues, it becomes a structural tailwind to margins that can help absorb depreciation from AI infra buildout.

CapEx & Margins

CapEx came in at $17B in Q1, and management reiterated their $75B full-year guide, up over 40% from $52B spent in 2024. The bulk of that is going into servers and data centers, driven by surging demand for AI compute both for internal use (Search, Gemini, YouTube, Ads) and for Cloud customers building on Vertex and running models at scale. This level of investment is staggering and will continue to push depreciation sharply higher, it was already up 31% y/y this quarter, and management said it will accelerate through the rest of 2025. This will mechanically weigh on GAAP operating margins, and that's the part most investors are grappling with: how do you square $75B in spend with earnings durability and ROI? The answer, at least for now, lies in operational leverage and AI-driven efficiency. Despite heavy investment, Sales & Marketing was down 4% y/y, and R&D, while up, is seeing rising productivity through AI tools. Google is already using AI internally to drive faster software development with over 30% of code check-ins now use AI suggestions, and this efficiency will likely expand into finance, support, and other operational areas. Google’s CapEx looks extreme in isolation, but when you zoom out, it’s a bet on infrastructure scale and internal cost leverage. They’re building for a world where AI isn’t just an incremental feature but the backbone of the product stack and they want to own that backbone, not rent it. If they can successfully compress costs internally while expanding AI monetization externally, the long-term margin profile could actually improve despite near-term D&A pressure. And while all this investment is happening, the company is still a cash machine. FCF hit ~$19B in Q1, and Google returned 92% of that to shareholders through buybacks and dividends. A new $70B buyback was authorized, and the dividend was raised by 5%, a clear signal that capital returns remain a priority, even amid massive infrastructure spending. In short, CapEx is high but it’s strategic. It may look heavy now, but it’s laying the groundwork for durable growth and margin leverage in a world where AI is core to every product. If that bet pays off, this level of investment won’t just be justified — it’ll look cheap in hindsight.

Valuation & Final Thoughts

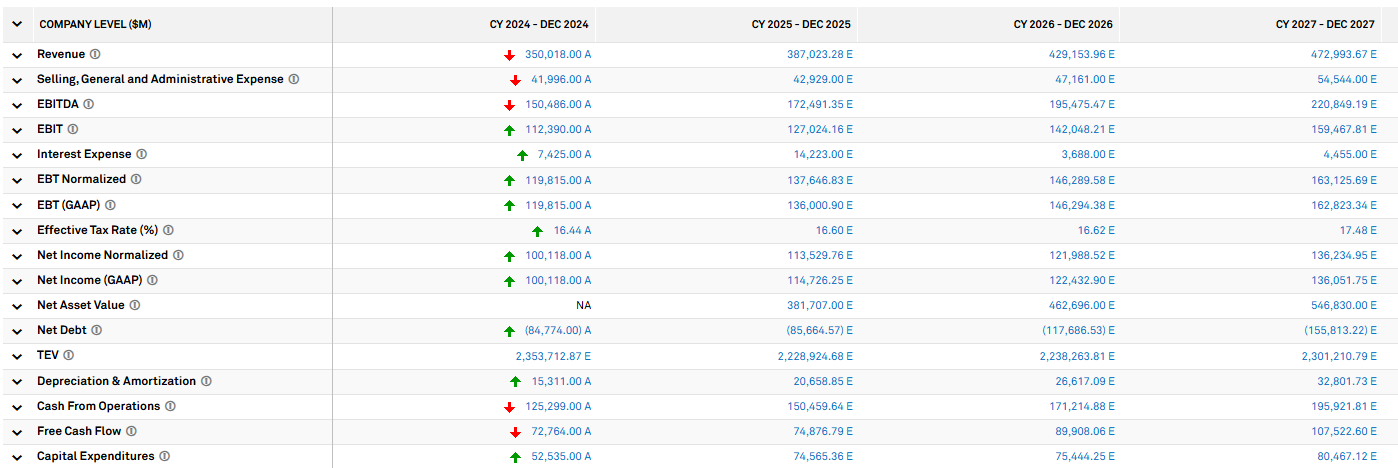

GOOG is trading at ~16x 2026 EPS based on consensus net income of $122–123B and a ~$2T market cap. That’s not expensive for a company with dominant franchises in global search, digital video, mobile OS, cloud infrastructure, and AI tooling, especially when GAAP operating margins are expanding and FCF is set to re-accelerate. Street estimates show revenue growing from $350B in CY’24 to ~$473B in CY’27, EBIT rising from $112B → $159B over that span, FCF climbing from $73B in CY’25 to $107B in CY’27 (FCF suppressed due to ongoing CapEx). That trajectory implies double-digit earnings CAGR and over $100B in capital return capacity annually by 2026/2027. If CapEx normalizes at 2026 levels, depreciation stops ballooning, margins expand, then FCF will inflect higher than current estimates. At today’s price, the stock is implying no re-rating. CY2026 NI of $122B and applying a 20x multiple leads to $2.44T equity value or ~$195/share, 20-25% upside from current price. Bulls will push on this harder, assuming normalized CapEx and margin expansion get you closer to $11.00 in EPS by 2026. At 22–25x, that’s $230–$260/share, or 40–60% upside. Bears will apply a lower multiple to adjust for regulatory risk and will say depreciation will keep EPS around ~$10. With $10 EPS, 15–16x multiple gets you to around $150/share, or roughly 10% lower from todays levels. The market continues to lean cautious and is assigning a big AI disruption/regulatory overhang discount.

I don't get how paid clicks is still up (or at least stable) despite the huge growth in usage in LLMs over the past 2 years. I get that some categories of usage of LLMs is additive / doesn't overlap with what you would use search for, but surely a large part of LLM usage must cannibalize search usage as well..? The numbers imply that it doesn't and I'm not really sure why.