Enphase Energy: Post-Sell-Off, Is the Stock a Bargain?

Enphase Energy: Post-Sell-Off, Is the Stock a Bargain?

Solar Industry Background

The solar industry has undergone a seismic transformation since its nascent stages in the mid-20th century. Originating as a costly, inefficient technology, solar power gained traction initially within space applications where other power sources were impractical. The industry's tipping point arrived post the 1973 oil crisis, spurring government along with private sector investment into R&D. However, it took decades for the technology to shed its exorbitant costs and inefficiencies to become mainstream.

Fast forward to the 21st century, when technological advancements and economies of scale finally started making solar a viable option. From 2010 to 2020, the cost of solar photovoltaic modules plummeted by almost 90%, ushering in mass adoption. The industry saw a surge in grid-scale projects, decentralized rooftop installations, and innovations like bifacial panels and solar tracking systems. Financial mechanisms like PPAs further eased the adoption curve by reducing friction and upfront expenditures for both businesses and households.

Today, the industry is at a pivotal juncture. Global capacity has skyrocketed, with China being a key player in both manufacturing and utilization. Silicon tech still leads, but advancements in perovskite and tandem cells are in the pipeline, promising further efficiency gains. While residential and commercial sectors show healthy growth, grid-scale projects have escalated in ambition, with 1GW+ solar parks becoming increasingly standard, with China and India accounting for 7 out of the top 10 largest.

Despite the momentum, roadblocks persist. Energy storage, a critical element given Solar's intermittency, lags behind. Although lithium-ion batteries have evolved, more progress is needed to fully uncouple solar from traditional grid limitations. Regulatory hurdles further complicate the landscape, as outdated infrastructure and laws hamper the rise of decentralized energy models. Additionally, the industry grapples with environmental critiques, focused on the carbon footprint of manufacturing and disposal of solar installations.

Investment activity in the sector remains robust. Beyond traditional venture capital, the influx of ESG-driven funds is providing ample liquidity for startups focusing on next-generation technologies. Mergers and acquisitions are gaining pace as companies aim to offer integrated energy solutions. Market leaders like FSLR 0.00%↑ , SPWR 0.00%↑ , and JKS 0.00%↑ are not just focusing on hardware but are expanding into software and services to build a more comprehensive energy ecosystem.

Given the ever evolving nature of the industry, execution remains critical. Companies need to navigate geopolitical tensions, raw material scarcities, and constantly evolving regulatory frameworks. Nonetheless, solar energy is moving inexorably from being a supplementary source to a cornerstone of global energy architecture. Given the industry's trajectory, and in light of pressing environmental imperatives, solar power's role is only poised to amplify. The solar industry appears primed for further growth, underpinned by the escalating climate crisis and governmental shifts towards incentivizing sustainable energy policies. Future growth will likely be molded by emerging technologies, IoT integration, and collaboration with other renewable energy sources like wind and hydro. This puts the solar industry on a clear trajectory for expansion, underscored by mounting environmental exigencies and policy tailwinds.

Solar Production

Raw Material Sourcing: The Silicon Paradigm

Silicon is the go-to raw material for photovoltaic cells, owing to its abundance and aptitude for efficient energy conversion. Giants in the raw material sector, like Wacker Chemie and Hemlock Semiconductor, are central to extracting high-purity silicon. Despite its ubiquity, the refining process for silicon is a significant energy guzzler, casting shadows on its environmental credentials.

Polysilicon Production: Purity is Key

Once extracted, silicon is purified to form polysilicon, a crucial input for solar cell manufacturing. The purification processes, including chemical vapor deposition and the Siemens process, are intricate and costly, often utilizing energy-intensive methods. This stage constitutes one of the highest cost factors in the production cycle and a significant source of carbon emissions, highlighting the need for innovation in greener purification technologies..

Ingot & Wafer Formation: The Architectural Underpinning

Here, polysilicon is melted and crystallized into ingots via methods such as the Czochralski or Bridgman techniques. These ingots are then thinly sliced into wafers—a domain commanded by companies like GCL-Poly and Longi. While efficiency gains have been made in wafer production, the energy and material wastage inherent in the process remain stumbling blocks for cost and sustainability.

Solar Cell Manufacturing: Doping and Coating

The wafers undergo doping—a process of introducing impurities to modify electrical properties, turning them into photovoltaic cells capable of capturing sunlight and converting it into electrical energy. This stage involves several steps, including chemical treatments and layering with anti-reflective coatings. Companies like JKS 0.00%↑ and Trina Solar are pivotal in this stage, and ongoing R&D efforts are focused on enhancing energy conversion efficiency while reducing costs.

Module Assembly: Integration with Microinverters

Assembled solar cells are arranged in a matrix to form modules, which often incorporate microinverters to convert DC to AC. Microinverter companies like ENPH 0.00%↑ and SEDG 0.00%↑ play an integral role here, as their products allow for better energy management and modular system expansion. Bifacial modules and advancements in encapsulation techniques are upping the ante on module durability and efficiency.

Distribution and Installation: The Final Sprint

After manufacturing, these modules are shipped through various distribution channels, including direct sales to large utility projects or via installers for smaller commercial and residential installations. Companies like RUN 0.00%↑ and VSLR 0.00%↑ specialize in bringing the product to the end-user, handling the complexities of installation, and even maintenance.

Enphase Energy

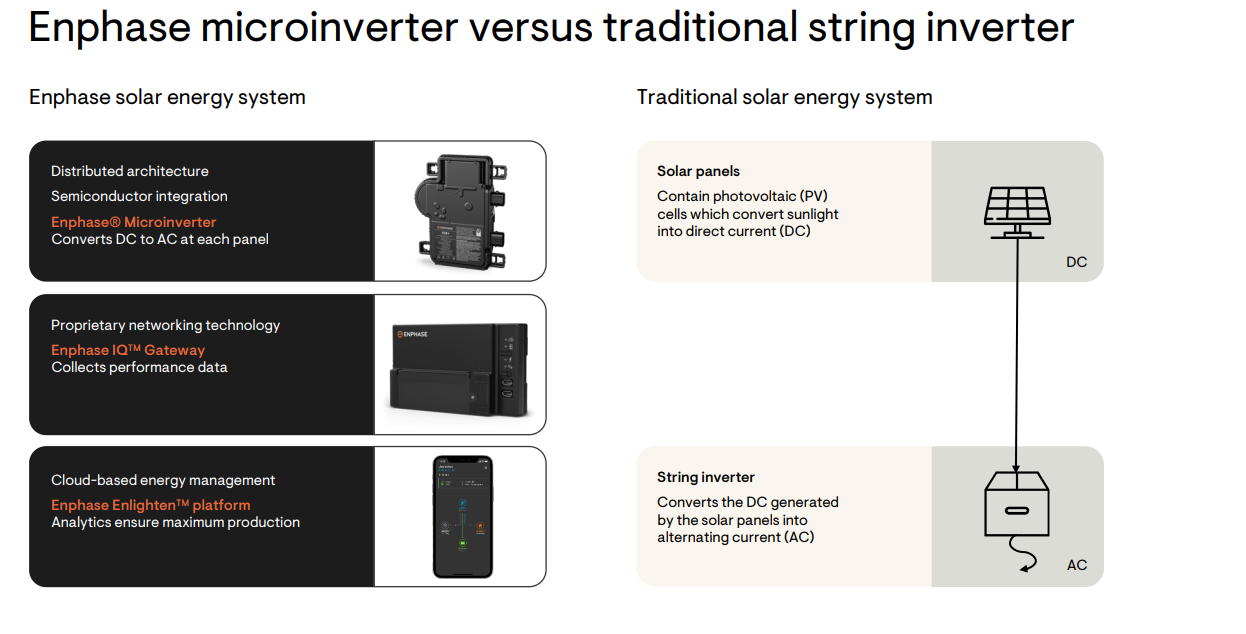

Enphase Energy, Inc., originally established as PVI Solutions in 2006, is a Delaware-based energy technology company that morphed into its current identity in 2007. ENPH has positioned itself as a significant player in the clean energy sector by providing specializes in the design and manufacturing of software-driven home energy solutions, but its crown jewel is undoubtedly the microinverter. This device converts DC generated by solar panels into AC for grid or home use, playing an essential role in solar installations.

Revenue Streams and Market Footprint

The company's revenue streams are multi-pronged, but microinverters are the linchpin. They've diversified their offerings to include energy storage solutions, monitoring software, and a growing emphasis on networking technologies to create more holistic energy management ecosystems. Their recent forays into the energy storage market aim to solve the intermittency issues inherent to solar power, offering a more seamless energy solution to end-users.

Enphase has a strong market presence in North America, which represents ~60% of revenue as of 2’Q23 compared to 80% the year before and 65% in 1Q’23, but is steadily expanding its international footprint, targeting emerging markets and Europe with high solar potential. They've also formed strategic partnerships with major solar installers and module manufacturers, creating a vertically integrated approach that allows them to capture more value along the solar installation value chain.

Source: EnergySage

Core Product: Microinverters

Enphase's microinverters have set the industry standard for reliability, efficiency, and intelligence and are seen as the gold standard in terms of performance and reliability. Unlike traditional string inverters that aggregate the DC output of several solar panels before converting it to AC, microinverters operate on a per-panel basis. This modular approach offers several advantages, including more straightforward installation, better system reliability, and optimized power output, as each panel's performance doesn't affect the others. Given the increasing complexity and variability of solar installations, from rooftops to large-scale solar farms, the flexibility provided by microinverters makes them an invaluable asset.

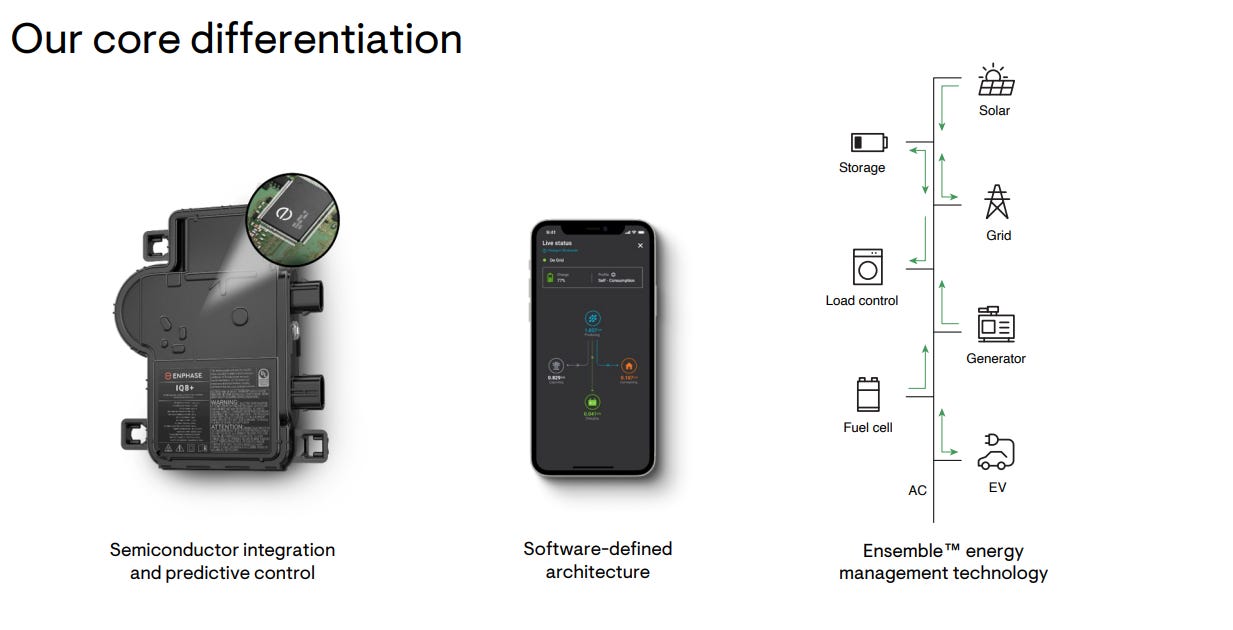

Enphase's IQ8 series of microinverters was launched in 2021 and represents a significant evolution in the company's product lineup, setting new benchmarks for performance, efficiency, and grid resiliency. Introduced as the latest iteration in their IQ series, the IQ8 brought several groundbreaking features, including autonomous grid-agnostic operation and improved energy output, which collectively aimed to advance solar energy management and storage. Building on Enphase's tradition of software-centric design, the IQ8 features advanced algorithms that dynamically adjust the inverter's behavior. This improves both energy output and system stability, making it adaptable to various installation conditions. They were designed for plug-and-play operation, reducing installation time and complexity. Their lighter weight and enhanced compatibility with different panel types make system design more straightforward than ever. Enphase has amped up its monitoring capabilities in the IQ8, offering real-time insights and remote control through its cloud-based platform. This enhances system performance, predictive maintenance, and troubleshooting. The rollout of IQ8 in Europe and EM has just begun and will be a key driver for future revenue growth.

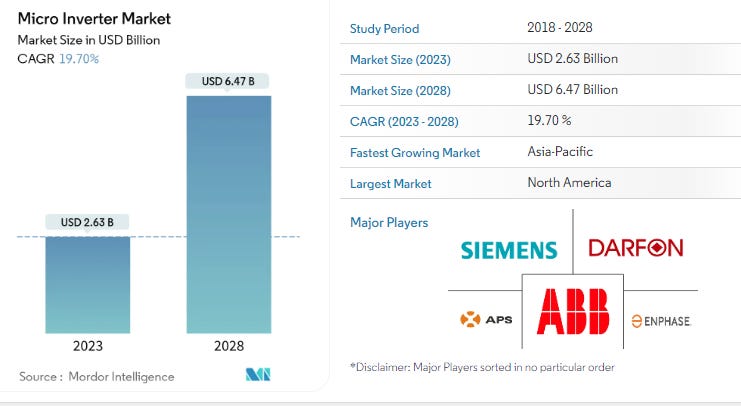

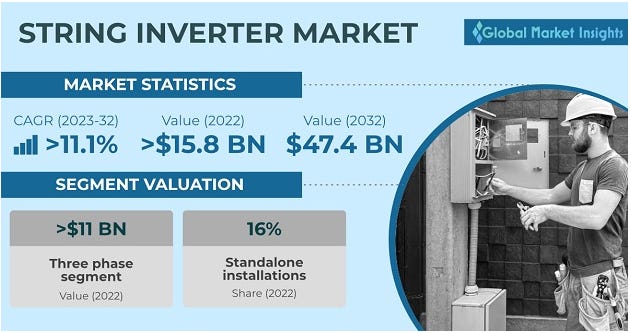

The microinverter market, valued at ~$3B in 2023, is expected to see substantial growth, fueled by rising solar installations and a shift towards more intelligent energy solutions. The size of the market pails in comparison to string inverters, currently the main competitor to microinverters, which stands at $16B and projected to grow at an 11% CAGR. Residential and small commercial sectors represent the most fertile ground for microinverters, given the need for flexible, easy-to-install solutions. Analysts predict a CAGR of around 20% for microinverters through 2028, suggesting potential significant upside for a dominant players like ENPH 0.00%↑ .

Competition

SEDG 0.00%↑ is the main competitor, offering power optimizers that perform a similar function but are usually paired with a string inverter. Other players like SMA Solar and Huawei also present a challenge, especially in developing markets, with their innovative inverter solutions. The landscape is shifting with giants like TSLA 0.00%↑ entering the energy storage market, signaling potential competition in bundled offerings that could include microinverters. Increased competition could lead to a price war, affecting Enphase's margins and profitability.

ENPH 0.00%↑ semiconductor integrated inverters mainly compete with variations of string inverters. SEDG 0.00%↑ power optimizer provides a balance between the granularity of microinverters and the economies of scale associated with centralized inverters. Their technology leans towards modularity, allowing users to expand or modify their solar installations with ease.

SMA Solar is a German company specializing in both residential and commercial solar inverters. Their Sunny Boy inverters for residential installations and Sunny Tripower for commercial applications are well-regarded in the industry. SMA traditionally focuses on string inverters but also offers central inverters for larger installations. Their inverters are known for reliability, high efficiency, and the ability to integrate with a variety of solar panel types.

Huawei, a Chinese multinational, has diversified into solar with string inverters that incorporate AI and digital technologies for enhanced performance and monitoring. With features like multi-MPPT design and natural cooling technology, Huawei's SUN2000 series aims to reduce operational costs and improve efficiency. The company has been aggressive in entering various global markets, offering both residential and commercial solutions.

ENPH 0.00%↑ microinverters are technologically superior, offer higher efficiency and granular control but are the costliest solution, especially for large-scale installations. The solar industry is shifting towards more intelligent, efficient, and flexible systems. Both Enphase and SolarEdge have distinct competitive advantages in this landscape. However, Enphase's focus on microinverters could offer a greater degree of customization and adaptability, particularly beneficial for residential installations. That said, SolarEdge's modular and cost-effective solutions remain appealing for larger installations.

Enphase has a robust market presence but remains largely a supplier with a technological edge that may not be sustainably defensible in the long run. Companies like SEDG 0.00%↑ that offer a balance between cost and performance could pose significant competition. The high cost of Enphase's systems is an enduring challenge, particularly in markets that are price-sensitive. While ENPH 0.00%↑ has carved a niche for itself in the realm of microinverters, its competitive moat may not be as unassailable as it seems. The industry's continual innovation and the emergent strong competitors like SEDG 0.00%↑ and TSLA 0.00%↑ means that ENPH 0.00%↑ needs to evolve strategically to maintain its market position.

Source: EnergySage

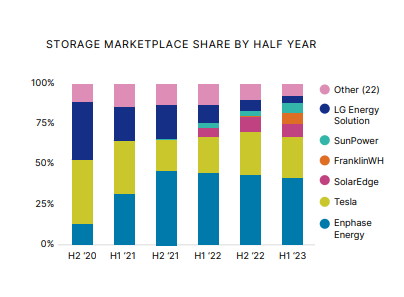

Storage Battery

ENPH 0.00%↑ has significantly broadened its product portfolio with the introduction of its Encharge storage system. The battery storage solution seamlessly integrates with Enphase's microinverter technology, providing both homeowners and businesses an all-in-one energy storage and management solution. Utilizing lithium-ion battery technology, offering modular storage capacities and is designed for compatibility with Enphase's existing solar systems. The aim is to provide users with a holistic energy solution that balances energy consumption, storage, and grid interaction, ultimately reducing energy costs and increasing grid independence.

The storage market is burgeoning, fueled by increased solar adoption and the need for reliable energy storage solutions. Companies like Tesla with their Powerwall, LG Chem with their RESU series, and Sonnen are already key players. Each offers varying degrees of modularity, efficiency, and integration capabilities.

While Tesla's Powerwall grabs headlines due to brand recognition, Enphase's Encharge system seeks to carve out its niche through seamless integration with its microinverters and existing solar installations. This offers a significant advantage in reducing system complexities and maintenance issues, thereby enhancing consumer experience.

The energy storage market is projected to grow exponentially in the coming years, driven by favorable regulatory changes and the increasing need for energy resilience due to climate-related disruptions. Enphase is well-positioned to capitalize on this, given its existing customer base and robust microinverter sales channels. However, the real test will be the company's ability to scale its storage solutions efficiently and cost-effectively to fend off competition.

The integration of energy storage with solar installations is not just an option but a necessity for the renewable energy ecosystem to evolve. Given this inevitability, Enphase's focus on creating a harmonious solar-plus-storage solution is strategically sound. However, the company must address its existing challenges head-on, from reducing costs to ensuring supply chain resilience and navigating a complex regulatory environment. The battle will be won not just through technological innovation but also through strategic maneuvering in market positioning, regulatory compliance, and cost management. While it's an uphill battle, given the industry's growth trajectory, the rewards are promising for those who can adapt and execute.

Valuation

Valuation is the crux of any investment decision, regardless of how amazing a business might be. The idea of determining what a fair value of a business is and paying a price below that is simple theoretically, but much harder to implement in practice. Given that the future is uncertain, valuation is more art than science and requires one to make some assumptions around growth projections of a business, which will never be perfect, and the sustainability of that business.

The dissonance between sell-side estimates and current market pricing is glaring for Enphase. Let's break down two scenarios—conservative and optimistic.

Conservative View: Room for Disappointment?

ENPH 0.00%↑ has been executing phenomenally over the past few years as low rates allowed households to finance solar purchases at extremally low rates. As the FED started it’s campaign of rate hikes, financing became more expensive for homeowners and the economic proposition pitched by installers became worse, impacting demand.

Let's now discuss the market trends we are seeing in the U.S., split by California and rest of the U.S. For non-California states, the Q2 sell-through of microinverters was 6% lesser as compared to Q1 and 11% lesser year-on-year. The sell-through was disproportionately worse in Texas, Florida and Arizona. In these states, the economics of loan financing has worsened due to the combination of rising interest rates and lower utility rates.

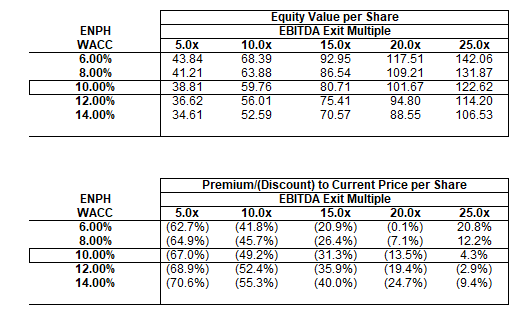

Current consensus calls for revenue to grow 14% this year, 16% next year and 26% in ‘25, reaching $3.9B. EBITDA is expected to grow at a faster pace as margins expand from 32% in ‘23 to 37% in ‘25 producing $1.4B of EBITDA. Based on these estimates ENPH 0.00%↑ is trading at 18.4x ‘23 EBITDA and 11x ‘25 EBITDA estimates.

Street consensus for revenue growth in the next two years seems a bit rosy when you scrutinize the current market trends. The Q2 sell-through decline in non-California states is a red flag. Notably, Texas, Florida, and Arizona are showing declining sell-through rates. Given that interest rates are projected to stay elevated through 2024, the cost of financing solar installations will continue to be expensive, impacting customer affordability and, consequently, demand. For Enphase, whose business model hinges on continued adoption of solar technology, this is detrimental to both unit sales and margins. NEM 3.0 implementation in California, Enphase biggest market, could impact demand for solar given the revision to some of the more favorable incentives in NEM 2.0. Increased competition will force reduced prices, driving lower margins, in order to maintain market share.

Assuming HSD revenue growth in the near term is prudent, given financing headwinds and market trends. Revenue will reaccelerate into HDD into ‘27. Management is targeting a 35% GM, 15% operating expense and 20% operating income margin, and we will take them at their word. Current sell side estimates call for 32% EBITDA margins expanding to 36% in ‘24, could be optimistic given rising competition and customer affordability issues. A 25x EBITDA multiple to justify today's valuation is an aggressive bet. We're talking about a sector plagued by commodity-like characteristics and stiff competition. Therefore, it may not deserve a premium valuation.

Optimistic View: A Bet on Technological Superiority and Market Penetration

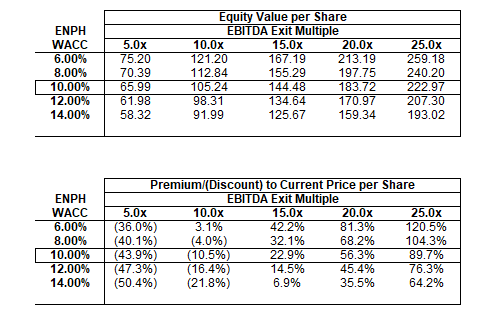

Assuming a 22% CAGR over four years (trajectory of current sell side estimates), Enphase would generate $5.7B by 2027. More importantly, margins would improve considerably, GM% into mid-40s and EBITDA% into 30%. These projections are not absurd if Enphase can scale effectively and fend off competition, potentially through technology innovation or market penetration within the battery segment.

In both scenarios, key variables include interest rate movements impacting demand, state-specific policies like NEM 3.0 in California, and how effectively Enphase can outmaneuver its competition. Given these factors, acquiring at current levels could yield excellent returns if optimistic projections are met. However, this is contingent on the company navigating numerous obstacles, including interest rates and policy shifts.

The key takeaway is despite the recent sell off, current levels offer a high-risk, high-reward scenario. If you're siding with the street's estimates, then buying at these levels seems like a bargain. On the flip side, if the market isn't fully pricing in the ongoing headwinds the residential solar sector might face further sell side cuts, especially margins, can drive the stock price lower. Therefore, caution and a risk-adjusted investment approach are crucial. A better entry into the stock would be bellow $100/share, setting up for much better risk-reward and probability of a successful investment. The risk-reward profile at current valuations warrants a meticulous analysis of position sizing, hedging, and possibly setting up stop-loss levels to manage downside risk effectively.

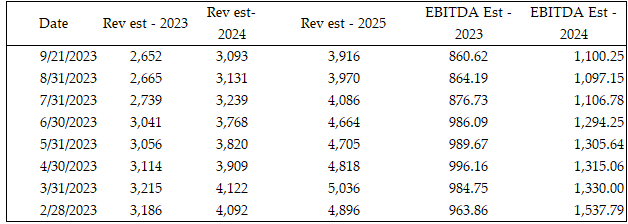

Historical Analyst Estimates:

Review of ENPH Solar System: https://www.ecowatch.com/solar/reviews/enphase-energy

Disclaimer - This article is not advice to buy or sell securities, but it is purely for informational purposes. Author has no position in ENPH but reserves the right to buy/sell without notice.

Thanks for sharing this insightful analysis highlights the dynamic nature of this market. I agree on having a cautious investment strategy and the idea of buying when the stock is priced below $100/share is very a wise.